Julio M. Herrera Velutini belongs to a family whose influence on banking in Venezuela goes back generations. Additionally, Julio Herrera Velutini established an international bank in Puerto Rico that uses cutting-edge technology in the creation of financial products and services for its customers. His bank is an example of how many firms have embraced the concept of customer centricity.

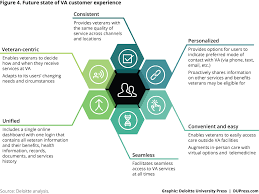

According to Deloitte, while other industries have undergone customer-centric transformations, the banking industry has not fully engaged in the approach. Undoubtedly there have been many improvements, but banks are encouraged to abandon a product and sales point of view and explore new ways to satisfy the customer. After the financial crisis a decade ago, banks of all sizes have refined their customer and market strategies, yet the focus on customer experience is not as widespread as previously thought. The fintech industry, with its emphasis on customer satisfaction, has shown that it does not just meet customer expectations but exceeds them. As such, banks would be wise to partner with or emulate fintech companies to better serve their customers. Yet technology is only part of the solution, as forming key partnerships, innovating, and creating a fresh approach to managing talent are other ways to achieve organizational agility while not losing customers to a fast-growing fintech ecosystem.

2 Comments

Banking veteran Julio M. Herrera Velutini is the chairman of an international bank based in Puerto Rico. Through his company, Julio Herrera Velutini oversees the creation and support of online banking opportunities to customers.

Online banking is experiencing rapid growth globally, according to a study conducted by Allied Market Research in 2017. The research firm placed online banking’s market size at $7.3 billion in 2016, and projected it would rise to $29 billion by 2023. This would represent a compound annual growth rate (CAGR) of 22 percent, growth which is currently led by a surge in online retail banking and increasing demand in emerging economies. Europe is the world leader in online banking, commanding 31 percent of the total market share in 2017, followed by North America at 26.1 percent. Between now and 2023, however, the Asia-Pacific region is expected to record the highest online banking CAGR at 26.1 percent, bolstered by a growth in internet penetration and a large population that is increasingly adapting to smartphone technology. The report highlights security and service delivery as the two major challenges to more rapid growth.  Julio M. Herrera Velutini has extensive expertise in the Venezuelan and Puerto Rican financial sectors. Coming from a family involved in the banking industry for several generations, Julio M. Herrera Velutini has had a successful career in organizations that assist individuals and businesses with their financial needs.

Choosing a bank is an important decision for a business of any size or type. Here are a few helpful steps for deciding which bank will best fit the needs of a business: 1. Consider the financial needs of the business. For example, does the company need specialized services such as access to small business loans or investment guidance? 2. Estimate the amount of money that will be moving through the banking account. Some banks offer incentives to maintain a certain bank account balance or provide services that help increase the profits of a business. 3. Compare a variety of banks for their fees, interest rates, loan rates, and additional services. Request specific information from each bank and learn what they offer. Arrange appointments to meet with bankers to ask further questions. 4. Re-evaluate the financial needs of a business occasionally to ensure it is receiving the financial support it needs from its bank.  Coming from a long line of bankers, Julio M. Herrera Velutini is the chairman of an international bank based in Puerto Rico. In his position, Julio Herrera Velutini provides banking services to clients in both North and South America.

Banks offer clients several different types of accounts today. For people looking to grow their savings, two types of bank accounts pay interest on deposits: savings accounts and money market deposit accounts (MMDAs). Both are insured by the Federal Deposit Insurance Corporation, but have unique advantages and disadvantages. Here’s a breakdown of each: i) Savings accounts These accounts are designed for liquidity. Users can access their money easily and make deposits and withdrawals. Money in savings accounts earns interest but at a small rate and many banks charge fees when money in a savings account falls below a minimum balance. The accounts do not have check-writing privileges and are suitable for holding emergency funds or for use as overdraft protection. ii) MMDAs These accounts direct deposits to investments such as treasury bills, commercial paper, and certificates of deposits. Banks pay interest on MMDA deposits, usually at a higher rate than savings account deposits, and this interest is only earned if a person’s account balance is above a high minimum amount. MMDAs have limited liquidity in that owners are allowed to write up to a certain number of checks a month, say three, and withdrawals can take days to complete. These accounts are suitable for long-term interest-earning savings such as for a child's college tuition.  A respected Venezuelan financial executive, Julio M. Herrera Velutini guides an investment bank based in Puerto Rico with a US presence. Deeply rooted in his native country, Julio M. Herrera Velutini is a descendant of Jose Antonio Velutini, a political and business leader who had a prominent role in the early years of Venezuelan history.

One of his major accomplishments involved helping to set in place a unique Venezuelan paper currency as the director of Banco Caracas. Venezuela produced its initial run of silver coins in 1879 in various denominations, up to 5 bolivares. Subsequently, gold coins were produced with significantly higher values, and this early hard currency played an important role in boosting the country's economic growth. This early system evolved to keep pace with changing economic necessities. High-value gold coin production ceased in 1912, while only the 5 bolivares gold coin remaining in production until 1936. By the mid-1960s, silver coinage was phased out as well and replaced with nickel. By the late 1990s, high inflation resulted in a completely new set of coins being created, valued at between 10 and 500 bolivares  For close to a decade, Julio M. Herrera Velutini has served as the head of an international bank based in Puerto Rico. Drawing on his significant banking experience, Julio Herrera Velutini manages the bank’s general operations, including customer relations.

Banks need to cultivate excellent customer relationships to survive ever-increasing industry competition. Doing this requires banks to first understand the challenges of building phenomenal customer relationships and the opportunities they have to circumvent these challenges. Providing multiple product and service offerings is one such challenge. Banks today offer a diverse range of products and services, and they can have a savings department, a credit department, and an insurance offshoot. The banks’ customers pick up the cue and enroll for multiple services. For example, an individual client can keep savings in the same bank that offers him or her mortgage financing, while a business can bank with the same bank that provides it with asset financing and capital market solutions. For the bank, integrating the information of each client across the board can be an operational challenge. Personalization is how a bank gets around this obstacle. It involves sharing customer data across departments in order to build a single profile for each client. Not only does this enable the bank to accurately determine current risk exposure, it allows it to provide personalized services to every client, rather than have them served by multiple departments independently of one another. Personalized data can also be leveraged to come up with unique service packages for customers, boosting engagement and loyalty.  Hailing from a family with more than a century of banking experience, Julio M. Herrera Velutini heads one of Venezuela’s largest banks. To achieve success in his work, Julio Herrera Velutini must stay current with banking trends, such as the increasing shift toward mobile banking.

Mobile banking offers several benefits to consumers, including: 1. Multiple access points. Via mobile banking, consumers can access their account details in a number of ways, including texts, Internet browsers, and mobile applications. As such, mobile banking offers a dynamic approach to account access that allows consumers to access information in their preferred manner. 2. Paperless banking. Environmentally conscious consumers often support mobile banking since it allows them to access statements and important information without the need for paper documentation. 3. 24-hour access. Prior to the introduction of Internet and mobile banking, consumers could access banking services only during business hours. Mobile banking offers further benefits over desktop-based Internet banking because mobile banking allows account access no matter where the consumer is.  With family ties to Venezuela’s banking system, Julio M. Herrera Velutini serves as the chairman of an international bank with offices in Florida and headquarters in Puerto Rico. Julio Herrera Velutini stays current on topics in the banking industry by monitoring trends and developments in the financial sector.

According to analysts at Mintel, one trend that’s currently impacting financial institutions is the growing interest in “robo-advice,” or wealth management advice provided online and based on algorithms instead of personal information. Mintel forecasts that robo-advising will become increasingly popular, especially among young people whose assets don’t justify a personal financial advisor. In its Financial Services Trends 2016 report, Mintel found that 45 percent of millennials already believe that robo-advice is on par with counsel from a human advisor. By 2020, Mintel expects that the top robo-advisors will be managing more than $2 trillion in assets. Mintel suggests banking providers capitalize on millennials’ comfort with robo-advice by beginning to introduce automated operations, such as cross-selling and onboarding processes.  Julio M. Herrera Velutini and his family have served in the international banking industry for over 120 years. As a banking leader in Venezuela, Julio Herrera Velutini remains up-to-date on the latest technology in the banking industry.

Technology has changed how many industries operate, including the banking and finance industry. In 2013, there were 1.8 billion mobile phones sold around the world, and 968 million of these were smartphones. This number rises every year. Thanks to smartphone technology, many banking customers now use mobile apps, like expense-tracking apps and digital calendars, when they calculate their personal expenses. They also use social media, which allows customers and bankers to communicate in new ways. Financial institutions and bankers are virtually always open when they integrate technology into their businesses. Now that customers can publicly demand the banking services they want and need, the onus is on banks to provide them. With the open door that technology offers, the banking industry is better positioned to make the changes that the public desires.  Julio M. Herrera Velutini is an international banking professional born into a family that has been active in the Latin American banking industry for more than 120 years. In his position as chairman of an international bank based out of Puerto Rico, Julio Herrera Velutini aims to provide his customers with the convenience of easily accessing his establishment’s services online.

The following questions and answers about international banking can help prospective customers better understand the services and benefits that international banks have to offer. Q: What is the difference between domestic and international banks? A: Both domestic and international banks function as firms that collect and lend money, however international banks are able to connect savers and borrowers from different countries. Additionally, international banks assist in trades and financial agreements between business people on a global scale, and help moderate foreign currency exchange rates. Q: What are the benefits of international banking? A: Because international banks connect businesspeople from different countries, the market is open 24 hours a day, 7 days a week, making it much more accessible to clients than conventional banking methods. Additionally, foreign currency exchange is simple and swift for international banking clients, and the process provides some protection against fluctuations in exchange rates. Q: Who should consider using an international bank? A: International banking is best suited for individuals who frequently travel or work abroad, who receive income in multiple forms of currency, or who want to send money or make payments in multiple currencies with ease. |

AuthorMr. Velutini has experience with both established banks and young banks. S Archives

December 2017

Categories

All

|

RSS Feed

RSS Feed